Thursday, October 28, 2021

Long-time NRIs, investors reveal how Indian expats should invest their savings in India

By Vijay Valecha in 'Century in News'

Vijay Valecha, Special to Gulf News October 28, 2021

Dubai: It's common for most non-resident Indians (NRIs) to remit their savings in Indian investment products for wealth generation.

However, picking the right instrument to park your hard-earned money is always of significant importance in order to make bigger financial gains.

Indian expat and 18-year-long UAE resident Sahitya K. Chaturvedi evaluates and classifies NRI investment opportunities as ‘good’, ‘better’ or ‘best’, based on his current expectations, investment size and time-period requirements needed for the investments. Chaturvedi is currently the head of accounts and finance at a Dubai-based company.

"Investing in mutual funds via SIP (Systematic Investment Planning) offer a higher return and lower risk. It is customisable in amount size and time period that makes it my most preferred investment option," explained Chaturvedi.

WHAT ARE SIPS?

A Systematic Investment Plan (or SIP) is an investment mode through which you can invest in mutual funds. As the term indicates, it is a systematic method of investing fixed amounts of money periodically. This can be monthly, quarterly or semi-annually etc.

Investment tip #1: Plan your investment strategy based on your needs, classifying them into short-term, long-term and lifetime options.

Chaturvedi classifies his investment strategy into short-term, long-term and lifetime strategies, which is within 6 to 12 months, 3 to 5 years and 10 to 15 years, respectively, when planning his investments in India.

"I ensure to keep updating my knowledge of capital markets and economic activities around the world to make informed decisions."

"For long term investments, real estate is my preferred choice. I have owned and invested in property in Mathura, Uttar Pradesh since 2003. Currently, I am exploring and evaluating real estate opportunities in Noida (Uttar Pradesh), Bengaluru (Karnataka), Gujarat and Mumbai with a long term investment horizon," he said.

"For mutual funds, I work with a five-year plan, as these help in keeping the balance between risks and returns. These include large-cap, multi-cap, ‘value-fund’, ‘focused-fund’, ‘balanced-advantage funds’ and ‘hybrid equity’, where one can acquire returns over the period ranging from 7 to 17 per cent. Some products I have invested in are Global Equity Alfa Fund, L&T Midcap Fund, Axis Triple Advantage Fund, Blue-chip ICICI, and Balanced Advantage Kotak."

GLOSSARY: ‘BALANCED-ADVANTAGE’, ‘HYBRID EQUITY’ FUNDS, ‘FOCUSED FUNDS’ AND ‘VALUE FUNDS’?

Balanced advantage funds (BAFs) are mutual fund schemes that invest in both equity and debt securities. Unlike regular hybrid equity funds, which keep allocation between equity and debt within certain prescribed limits, BAFs have no such limits and move their allocations more dynamically.

A focused fund is a mutual fund, which holds a relatively small number of stocks or bonds in some dimensions that are identical. Through definition, in a limited number of sectors, a concentrated mutual fund focuses on a limited number of stocks rather than holding a large or varied mix of positions.

A value fund is a pooled investment that follows a strategy focusing on shares that are undervalued based on fundamental analysis. Value stocks are frequently well-established companies that offer investors dividend payments. Warren Buffett, one of the world's most successful investors, is a value investor.

"Equity trading, I usually do to gain the short-term benefits. For equity stocks, my selection goes towards sectors like IT, education, banking, and infrastructure, wherein the short-term returns allow me to gain an average of 30 per cent returns. Infosys, Tech Mahindra, Bharti Airtel, SBI, HDFC, HCL Tech, ITC, Cipla, ONGC, NIIT are some of the products that offered me great returns.

"I am also exploring opportunities in Tata Motors, Reliance Industries, Dabur, Glaxo, Facebook, ICICI Prudential Fund as these offer some high return investments options."

Investment tip #2: Review your investment strategy regularly and amend the plan according to changing market trends.

Chaturvedi has subscribed to publications and research material from three investment banks, based on their headquarters, local presence in Dubai, and the size and type of product portfolio in capital and insurance markets. He is a regular follower of their daily, weekly and monthly research and does his study from the open resources.

He finds it interesting to see how several opinions vary from one report to another, but few similarities direct him to identify and evaluate his choice.

He further pointed out that the volume of analytics, recommendations, supportive articles, and statistical tools offered in these reports is highly fragmented. Hence, he suggested that every investor must follow authentic research and never make investment decisions influenced by social influencers.

He uses stock market chart and analysis tools like ‘Moving Average’, ‘Candlesticks’, ‘Bollinger bands’, ‘Parabolic’, ‘T-Points’, and ‘risks index’ to monitor daily trading trends in the live market. (Link to YM story explaining each of these)

Investment tip #3: Plan your India investment exposure based on your retirement goals.

Siddarth Razdan, who has lived in the UAE for 18 plus years, said NRIs need to plan their India investment exposure depending on whether they want to retire in India or overseas and have family commitments in Indian Rupees. Razdan is a Chartered Accountant who is currently part of the management team at India-based First Bridge Fund Managers.

He added, "When an NRI wants to retire in India, then he or she should have an overall allocation of 70 per cent in rupee-denominated products gradually going up to 90 per cent nearing retirement. However, suppose an NRI is settling overseas and has limited fund requirements in the Indian rupee. In that case, a 50 per cent allocation should be in India equally split between Rupee and Dollar denominated India investments."

He further said that those planning to retire in India eventually should take a basic family medical insurance cover of Rs500,000, so no claim bonus is accumulated. This way, he said, they do not face a spectre of high medical insurance premiums when they relocate to India on account of the age factor.

"It would also be worthwhile to explore a term policy denominated in Indian Rupees as life insurance premiums have become reasonable recently because of COVID-19, while one may expect a spike in Insurance premiums globally."

Investment tip #4: Be clear on your risk appetite to determine the right product for investments.

Razdan also recommended NRIs with a high-risk, high-return appetite to consider investing small amounts starting as low as Rs500,000 in promising start-ups through platforms like Venture Catalysts Lets Venture and many others.

However, Razdan also cautioned NRIs about the possibilities of losing 100 per cent of capital invested in such products. “But the returns of such investments could also be extraordinarily high,” he explained.

"Those who want high returns but can’t take on not-very-high risk could also explore Alternative Investment funds focused on Venture Debt, which has become popular in recent years with ultra-high net worth individuals (‘UHNIs’ i.e. people with a net worth of $30 million or Dh110 million and above) in India."

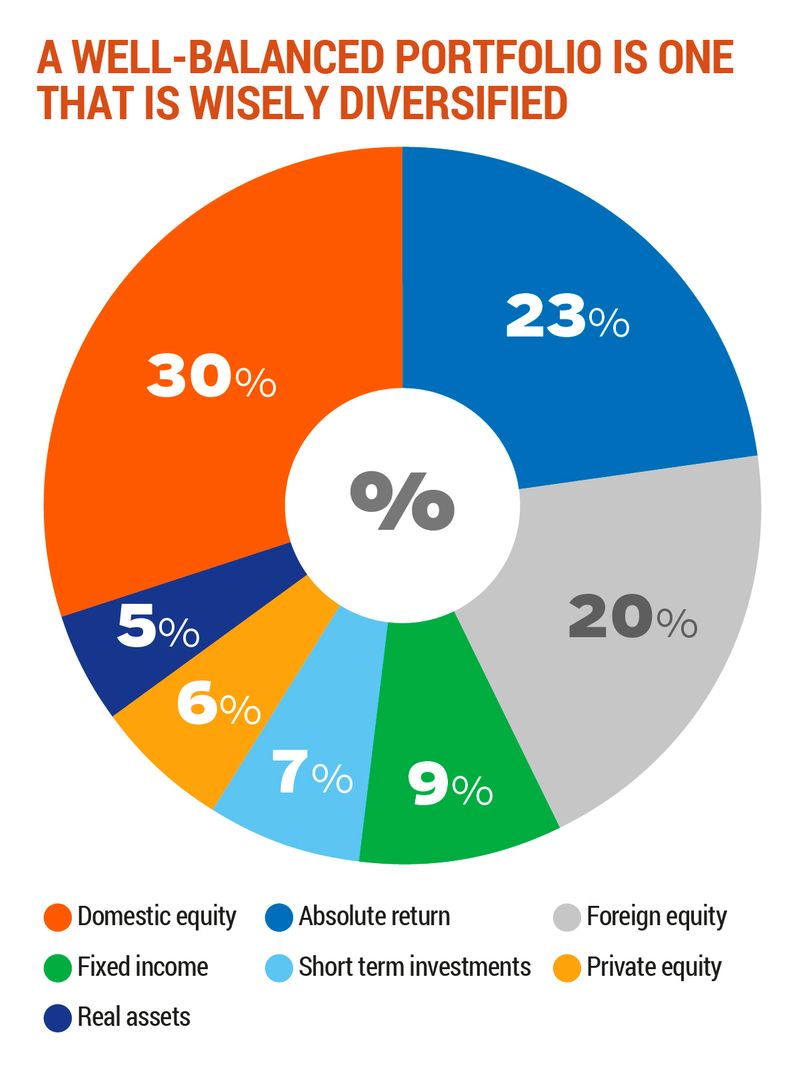

"Overall Index funds could also be used as a low-cost option for equity exposure. It is recommended that one should not have too many schemes, and one or two large caps, one mid-cap and one Flexi and one index fund are ideally recommended in equity exposure. Equity exposure recommended would be 60 to 80 per cent with equity exposure going down with age."

GLOSSARY: WHAT IS A FLEXI FUND AND AN INDEX FUND?

Flexi-cap funds are those funds which invest in companies across the market capitalisation spectrum, i.e. large-cap, mid-cap, and small-cap stocks.

An index fund is an investment that tracks a market index, typically made up of stocks or bonds. Index funds typically invest in all the components that are included in the index they track, and they have fund managers whose job it is to make sure that the index fund performs the same as the index does.

"Those NRIs who have direct equity exposure should have 60 to 80 per cent allocation given to large-cap stocks and 20 per cent to the mid-cap. One could also explore options as Alternative Investment Funds (AIFs), which focussed on private equity venture capital listed companies, but these are recommended for HNI (high net worth) NRIs only as some of these are products have a long lock-in as high as 5 to 10 years."

Investment tip #5: Go for Capital Guarantee Solution, a market-linked plan with no risk to capital.

A Capital Guarantee Solution plans blend Unit Linked Investment Plans (ULIPs) (YM story on ULIPs) and guaranteed return plans. Vivek Jain, head of investments at PolicyBazaar.com said, "These products promises complete security to your invested amount apart from offering upside of the market. This means, no matter how bad the market performs, your invested amount is completely secured.

"In these plans, around 50-60 per cent of the invested amount goes into guaranteed return component, and the rest goes into ULIPs. These plans also offer a life cover paid to the dependents on the death of the policyholder. Usually, the life cover is ten times your annual premium or 120 times of your monthly premium.

"These plans also give better returns compared to fixed deposits (FDs) and debt mutual funds apart from tax benefits. A Unit Linked Insurance Plans or ULIPs over 15 to 20 years can promise returns as high as 15 per cent."

Investment tip #6: Exchange-traded funds are ideal for building a diversified portfolio, considering the relatively low investment amounts.

VALECHA RECOMMENDS THE BELOW ETFS AN INDIAN EXPAT CAN CONSIDER WHEN INVESTING IN INDIA:

- SPY SPDR ETF: SPY is the most well-known and oldest in terms of assets under management (AUM) and trading volumes. Companies like Microsoft, Apple, Amazon, Facebook, JPMorgan, and Alphabet (Google) are included. The annual returns of the ETF are 20.8 per cent.

- QQQ Powershares ETF: QQQ tracks the NASDAQ 100, a list of some of the world's most innovative companies, including Google, Tesla, Starbucks, Netflix, eBay, and Intel. The annual returns of the ETF are 19.2 per cent.

- Nifty India Financials ETF: The index is designed to measure the performance of companies in the Indian financial market, including banks, financial institutions, housing finance, and insurance companies. The annual returns of the ETF are 20.5 per cent.

- Kotak Nifty 50 Index Fund: The scheme's investment objective is to replicate the composition of the Nifty 50 and generate returns that are commensurate with the performance of the NIFTY 50 Index, subject to tracking errors. The annual returns of the ETF are 20.4 per cent.

Gulf News

__565361333.jpg)

__1702287518.jpg)

__1239930142.jpg)

__396687930.jpg)

__196023842.jpg)

Regulated by SCA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Securities and Commodities Authority (SCA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.