Thursday, September 24, 2020

Snowflake’s IPO: Are there any gains left for regular investors?

By Century Financial in 'Brainy Bull'

Snowflake's [SNOW] IPO last week was huge. So huge that in the space of a single day Snowflake’s share price jumped 112%, doubling the value of early backers’ shares, who had been allocated them at $120 a pop. By the end of the day, Snowflake’s share price was trading at $245, giving it a market cap of $71bn.

So have retail investors missed out by skipping Snowflake’s IPO, or are there more gains to come?

What happened during Snowflake’s IPO?

For early backers, Snowflake's soaring share price is a win, even if it did drop 10% the day after going public. Among those initial investors are Berkshire Hathaway and Salesforce, each picking up $250m worth of stock at Snowflake’s IPO.

Yet for the retail investor, this isn’t necessarily a good thing. Like all companies, when the cloud data firm went public, it offered stock to institutional investors at Snowflake’s IPO price via an investment bank. Retail investors have to wait until a stock goes public to pick up shares. So when Snowflake's share price jumped, it was the institutions who profited, rather than everyday investors.

Retail investors aren't the only ones who might have missed out on Snowflake’s IPO. The fact its share price doubled so quickly means it could have been undervalued at the time of the IPO, suggesting it might have left some money on the table.

According to CNBC, if Snowflake’s IPO had been priced closer to the amount the broader market was willing to pay, it could have made $3.8bn. That's on top of the $4bn Snowflake made in its IPO and private placements.

Is Snowflake’s share price a buy?

Cloud-based Software as a Service offerings aren't anything new — Amazon [AMZN], Microsoft [MSFT] and Alphabet [GOOGL] all offer similar services — but what makes Snowflake different is that it can run on any of these cloud platforms. That’s a unique selling point as companies often use more than one provider for their cloud services.

Snowflake can also be scaled up or down as needed, which means it can charge depending on usage, rather than a flat fee. This has seen Snowflake add new clients at a remarkable rate. Last year it upped its client count from 948 to 2,392, while this year it has added 800 more, taking the total above 3,100.

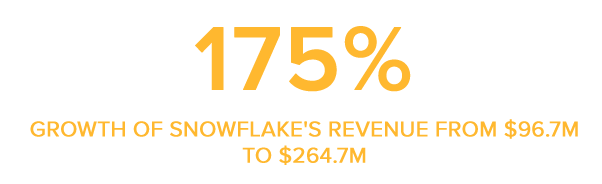

Revenue growth has also been strong, jumping 175% in the year ending 31 January, from $96.7m to $264.7m. Sales in the first six months of 2020 have been similarly promising, going from $104m to $242m.

However, losses have also grown to $348.5m compared to the last fiscal year’s $178m. According to the Financial Times’ Richard Waters, the scale of the IPO is out of sync with the company's fundamentals:

“...a market valuation of about $70bn after the first day of trading — or 140 times its current annualised revenues, and nearly six times what the company was judged to be worth in a private fundraising round earlier this year — is head-scratching.”

Beyond Snowflake’s IPO, Waters highlights the competition that the firm will face from Amazon, Google and Microsoft, which already have a formidable hold on the market and aren’t known for playing nicely with the competition.

Where next for Snowflake’s share price?

Since Snowflake’s IPO, its share price has oscillated between $240 and $220 and closed 22 September at $235.16. Whether it can continue to add new customers while fending off the competition remains to be seen. For investors, it could be worth waiting for the heat around Snowflake’s IPO to die down before taking a considered position on the stock.

As CMC analyst Michael Hewson explains:

“The big question now in an age of big data is whether Snowflake can continue its recent stellar progress, and growth of new clients, or whether the interest that’s been shown in the past few days starts to melt away.”

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by SCA

Century Financial Consultancy LLC

Dubai Polo & Equestrian Club

The Official Partner of

Dubai Polo & Equestrian Club

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

Office 3014, 30th Floor

Tamouh Tower, Building 12, Marina Square,

Al Reem Island, Abu Dhabi - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries risk. Trading in leveraged Over-The-Counter (OTC) Derivative products (including Contracts for Difference (CFDs) and spot foreign exchange contracts) involves a significant risk of loss which can exceed deposits and may not be suitable for all investors. OTC Derivative products / CFDs are complex financial instruments that do not confer any claim or right to the underlying financial instrument. Transactions in these instruments are very risky, and you should trade only with the capital you can afford to lose. Before deciding to trade on these products, you should consider your investment objectives, risk tolerance and your level of experience. Accordingly, you should ensure that you understand the risks involved and seek independent advice from professionals, if necessary.

Century Financial Consultancy LLC (CFC) is duly licensed and regulated by the Securities and Commodities Authority of UAE (SCA) under license numbers 20200000028 and, 20200000081 to practice the activities of Trading broker in the international markets, Trading broker of the OTC derivatives and currencies in the spot market, Introduction, Financial Consultation and Financial Analysis, and Promotion. CFC is a Limited Liability Company incorporated under the laws of UAE and registered with the Department of Economic Development of Dubai (registration number 768189). CFC has its registered office at 601, Level 6, Building no. 4, Emaar Square, Downtown, Dubai, UAE, PO Box 65777.

Any content available on our website is presented solely to provide information and educate visitors. Under no circumstances is any of this content meant to be construed as an offer, recommendation, advice, or solicitation to buy or sell securities or other financial products.

This website's information is not intended for use by anybody residing outside UAE or where such use would violate local laws or regulations.