Wednesday, July 15, 2020

How will Uber's share price fare in the food delivery wars?

By Century Financial in 'Brainy Bull'

Uber’s [UBER] share price has had something of a turbulent year so far in 2020. It has struggled to regain the $45 at which it debuted in May last year, despite coming close on 12 February with an intraday high of $41.86, before dropping slightly to close at $41.25.

It then plummeted 64% to an all-time low of $14.82 on 18 March amidst the coronavirus panic, before recovering throughout April and May. June saw less positive news for Uber’s share price, however, and it ended the month 13.23% below its closing price on the 1 June.

As of 13 July’s close, Uber's share price is up 2.36% year-to-date at $31.72. This climb has been fed in large part by the company’s deal to acquire delivery startup Postmates for $2.65bn.

Will the deal be enough to keep driving Uber's share price, or are there more bumps in the road ahead?

A new roadmap for Uber’s share price

Amid international lockdowns, Uber’s share price has benefitted from a shift in its core business from ride-hailing to food delivery — a market that CEO Dara Khosrowshahi had previously suggested the company would leave, The Wall Street Journal reports.

Due to increased demand for food delivery in recent months, Uber has been looking to grow its operations by buying out the competition.

The company had initially been in talks to take over Grubhub [GRUB], but the deal fell through after months of negotiations. Grubhub has since signed with European behemoth Just Eat Takeaway [TKWY] for $7.3bn. Unsurprisingly, Uber’s share price dropped 16.13% in less than a week following this news, closing at $31.10 on 10 June.

Uber’s share price has remained around the $30 level since. Following news that the company will acquire Postmates in an all-stock deal, the company’s share price surged 5.9% on 6 July. The stock has declined again since, settling back to $31.72 through 13 July’s close.

To finance the purchase, Uber estimated it would need to issue about 84 million shares, which makes the deal worth circa $2.65bn.

Taking on the competition

Postmates is one of the smallest players in the US food delivery sector, with an estimated market share of 7% in April, according to data by Edison Trends.

The firms expect an Uber and Postmates partnership to control about 37% of the US market, putting them second-place to US giant DoorDash, which controls 45% of the market share.

In an email sent to staff in May, Khosrowshahi stated that the Uber Rides business was down circa 80%. Meanwhile, Uber Eats' bookings more than doubled in Q2, with Postmates' orders growing 67%, according to CNBC.

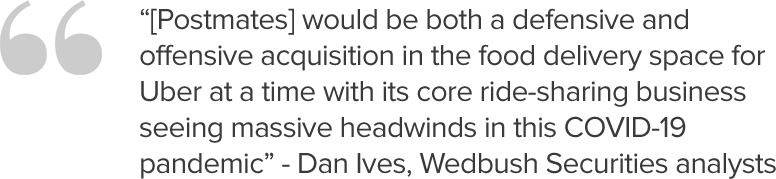

"[Postmates] would be both a defensive and offensive acquisition in the food delivery space for Uber at a time with its core ride-sharing business seeing massive headwinds in this COVID-19 pandemic," Dan Ives, an analyst at Wedbush Securities, told NPR.

What do the analysts think?

Among 42 analysts polled by CNN Money, Uber's share price has a consensus buy rating from 32 analysts. Meanwhile, six rate the stock a hold and three give it an outperform rating, while just one analyst suggests to sell.

Among the 38 analysts offering 12-month price forecasts for Uber, also polled by CNN Money, there is a median target of $40.50. This would see a 27.7% upside on Uber’s current share price.

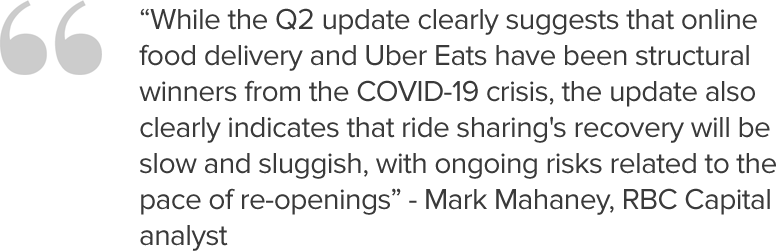

Mark Mahaney, an analyst at RBC Capital, has an outperform rating on the stock, according to Barron's. However, he recently cut his target price from $52 to $45, in order to reflect the adjustments in his earnings outlook for the company.

"While the Q2 update clearly suggests that online food delivery and Uber Eats have been structural winners from the COVID-19 crisis, the update also clearly indicates that ride sharing's recovery will be slow and sluggish, with ongoing risks related to the pace of re-openings,” Mahaney stated.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by SCA

Century Financial Consultancy LLC

Dubai Polo & Equestrian Club

The Official Partner of

Dubai Polo & Equestrian Club

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

Office 3014, 30th Floor

Tamouh Tower, Building 12, Marina Square,

Al Reem Island, Abu Dhabi - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries risk. Trading in leveraged Over-The-Counter (OTC) Derivative products (including Contracts for Difference (CFDs) and spot foreign exchange contracts) involves a significant risk of loss which can exceed deposits and may not be suitable for all investors. OTC Derivative products / CFDs are complex financial instruments that do not confer any claim or right to the underlying financial instrument. Transactions in these instruments are very risky, and you should trade only with the capital you can afford to lose. Before deciding to trade on these products, you should consider your investment objectives, risk tolerance and your level of experience. Accordingly, you should ensure that you understand the risks involved and seek independent advice from professionals, if necessary.

Century Financial Consultancy LLC (CFC) is duly licensed and regulated by the Securities and Commodities Authority of UAE (SCA) under license numbers 20200000028 and, 20200000081 to practice the activities of Trading broker in the international markets, Trading broker of the OTC derivatives and currencies in the spot market, Introduction, Financial Consultation and Financial Analysis, and Promotion. CFC is a Limited Liability Company incorporated under the laws of UAE and registered with the Department of Economic Development of Dubai (registration number 768189). CFC has its registered office at 601, Level 6, Building no. 4, Emaar Square, Downtown, Dubai, UAE, PO Box 65777.

Any content available on our website is presented solely to provide information and educate visitors. Under no circumstances is any of this content meant to be construed as an offer, recommendation, advice, or solicitation to buy or sell securities or other financial products.

This website's information is not intended for use by anybody residing outside UAE or where such use would violate local laws or regulations.