Wednesday, December 09, 2020

Will Salesforce acquisition boost Slack’s share price?

تم إعداد هذا المنشور من قبل سنشري للاستشارات

Reports that Slack [WORK] is set to be acquired by Salesforce [CRM] for a record-breaking $27.7bn pushed Slack’s share price to its highest level since 20 June 2019 — its public debut. With the company having announced its Q3 2021 earnings a week earlier than expected on 1 December, what’s in store for Slack’s share price?

Until news of the acquisition broke on 25 November, Slack’s share price had been beaten down and was 14% off its then-52-week high of $42, set in June. Since the Wall Street Journalreleased its exclusive report on the acquisition, Slack’s share price has soared 44.29% (as of 7 December’s close).

On 1 December, Slack’s share price hit an all-time intraday high of $44.15 before closing at a high of $43.84. As of 7 December’s close, Slack’s share price has gained an impressive 85.4% year-to-date and is 182.65% above its 52-week low of $15.10, recorded on 16 March.

Strong numbers, but struggling

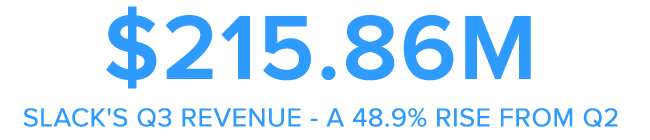

For the three months to the end of July, Slack reported revenue of $215.86m, up 48.9% from the $144.97m generated in Q2 2020. Its net loss of $74.85m was a significant improvement on the $359.56m loss reported in the year-ago quarter, and its EPS was $0.00. The earnings beat analyst expectations, according to Refinitiv data.

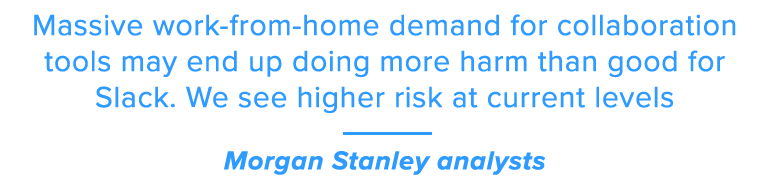

Despite signs of strength in these numbers, Slack’s share price has struggled of late. Between the market correction in early September and news of the Salesforce deal, the stock was down circa 11%. The release of a report by Morgan Stanley towards the end of October didn’t help — this declared that Slack was no longer a beneficiary of the work-from-home trend, with potential customers choosing rival products, including Microsoft [MSFT] Teams and Zoom [ZM].

“Massive work-from-home demand for collaboration tools may end up doing more harm than good for Slack. We see higher risk at current levels,” wrote analysts at Morgan Stanley, who downgraded the stock from equal weight to Underweight and set a price target of $27.

The earnings report for the third-quarter fiscal year 2021, released by the company on 1 December, showed revenue of £234.5m, up 39% year-over-year on the $168.72m revenue reported in Q3 2020. According to Zacks Equity Research, five analysts had forecast revenue to be in a range of $231.93m–$238.3m, with a consensus of $234.67m.

Reducing customer churn

In its most recent 10-Q filing, Slack CEO Stewart Butterfield cited business budget cutbacks as a reason for customer churn: paid customers were deciding not to renew their subscriptions.

As of the end of 2Q21, Slack had 130,000 paying customers, up 30% year-over-year. In the first quarter, the company had reported having just over 122,000 paid customers — adding 12,000 in the three months to the end of April, up 28% from Q1 2020.

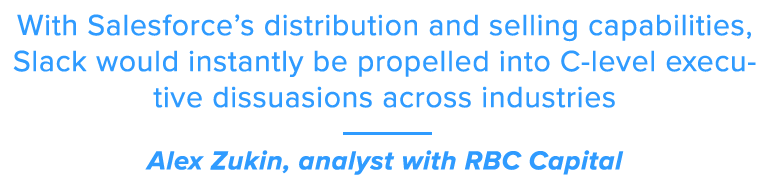

The third quarter’s results show paid customers have turned their backs on Slack for more attractive, bigger-name products like Microsoft Teams and Zoom. However, analysts suggest the Salesforce deal could be a boon for Slack further down the road.

“With Salesforce’s distribution and selling capabilities, Slack would instantly be propelled into C-level executive dissuasions across industries,” Alex Zukin, analyst with RBC Capital, wrote in a note to clients seen by CNBC.

Slack currently has 21 Wall Street ratings, according to MarketBeat, of which four are Buy, 15 Hold and two Sell. The consensus price target is $39.68, which represents a 7.03% drop from Slack’s share price at close on 7 December.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

تنظمها هيئة الأوراق المالية والسلع

سنشري للاستشارات المالي ش.ذ.م.م

تصل إلينا:

-

دبي

الطابق رقم 6, مبنى رقم 4, ساحة إعمار دبي

وسط مدينة دبي، ص.ب: 65777،

دبي، الإمارات العربية المتحدة -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Century Financial is the presenting sponsor of

ينطوي التداول في المنتجات المالية على مخاطر كبيرة. فالاعتماد على المشتقات المالية المتاحة للتداول خارح البورصة، مثل عقود الفروقات وتداول العملات الأجنبية (الفوركس) الفوري، قد يتسبب في خسائر تتجاوز قيمة الإيداعات الأولية، مما يجعلها غير ملائمة لجميع المستثمرين. فهذه الأدوات المالية المعقدة لا تمنح ملكية مباشرة للأصول الأساسية. لذا، ينبغي للمستثمرين الاحتراز عند تحديد أهدافهم الاستثمارية ومراعاة مستوى المخاطرة المتوقَع، واللجوء إلى الاستشارة المهنية المتخصصة عند الضرورة.

سنشري للإستشارات والتحليل المالي ش.ذ.م.م (الشركة)، شركة مرخّصة ومنظمة من هيئة الأوراق المالية والسلع في دولة الإمارات العربية المتحدة، بموجب الترخيص رقم (20200000028) و(301044) لتولي أعمال الوساطة في الأسواق الدولية، وتداول المشتقات المالية والعملات المتاحة للتداول خارج البورصة في سوق التداول الفوري، بالإضافة إلى تقديم الخدمات الاستشارية والترويجية. تأسست الشركة بموجب قوانين دولة الإمارات العربية المتحدة، وهي مسجلة لدى دائرة التنمية الاقتصادية بدبي (رقم: 768189)، حيث يقع مكتبها المسجّل في 601، الطابق السادس، المبنى رقم 4، ميدان إعمار، وسط مدينة دبي، دولة الإمارات العربية المتحدة، ص.ب. 65777.

لا يُعرَض محتوى هذا الموقع الإلكتروني إلا لأغراض تعريفية تثقيفية بحتة، فلا يمثل عرضًا ولا توصيةً ولا دعوةً لشراء أو بيع أي أوراق مالية أو منتجات مالية.

لا تنوي الشركة استخدام أو توزيع منتجاتها وخدماتها في أي ولاية قضائية حيث يُشكِّل هذا الاستخدام أو التوزيع انتهاكًا للقوانين المحلية أو اللوائح التنظيمية.